EPM Contradicts Ex-Governor Luis Perez’s Claims of ‘Disastrous’ Expansion Strategy

Medellin-based electric power and utilities conglomerate EPM is publicly clashing with former Antioquia Governor Luis Perez (2016-2019) over a 15-years-long, debt-financed expansion strategy that has catapulted EPM from just another a local utility to a multinational giant.

“From the path traced in 2006, EPM has become a business group that today has 14 affiliates and 30 subsidiaries, which has allowed it to become one of the main Latin American multinationals” — and simultaneously funds around 25% of Medellin’s annual city budget from its annual profits, EPM notes.

It’s an extraordinary business model — created in a city noted for a tradition of entrepreneurship, not only in the private sector but also — spectacularly so — in the public sector.

But such expansion has come with growing and even dangerous debt loads, according an August 20, 2020 opinion column written by former Governor Perez for the national business newspaper, La Republica.

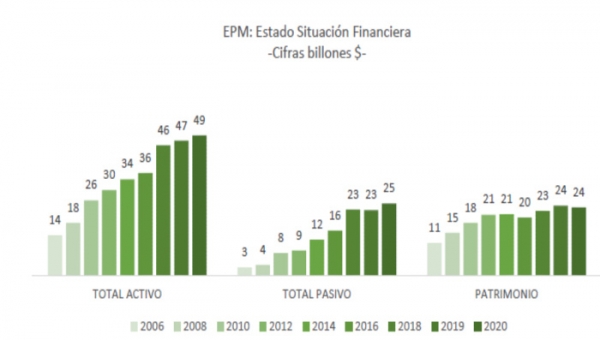

“Until 2013 the company [EPM] had an equity much higher than its liabilities,” according to Perez. “After 2013, liabilities began to grow without limits, exceeding their equity, and by 2020 the company that their executives and their boards claim to defend so much has a burden of liabilities so great that it lost its strength.

“As of 2020, EPM has a net worth of COP$23.7 trillion [US$6.18 billion] with a very high liability of COP$33.6 trillion [US$8.76 billion],” Perez claims — although this claim is contradicted in EPM’s latest filing with Superfinanciera (see chart, above, showing COP$24 trillion (US$6.25 billion) net equity, rather than a negative asset/liability balance).

“In 14 years, the net worth only multiplied by two times, while the scandalous liabilities multiplied by 13 times. If EPM remains the same in the next 15 years, it could go bankrupt or disappear,” Perez claims.

Since embarking on international expansions, EPM’s investments “are generally a disaster and many describe them as a bad example of international corruption and business inefficiency,” Perez claims, citing allegedly negative net-present-values (NPVs) in EPM investments in HET (Panama), Ticsa (Mexico) and Cururos (Chile).

“In Panama, not only the hydroelectric plant had scandalous cost overruns of US$150 million,” but the Cururos NPV target “was not met and the it actually made a loss of US$111.2 million,” according to Perez.

“If Hidroituango’s construction errors [which Perez claims caused the diversion-tunnel collapse in 2018] add-up to COP$9.9 trillion [US$2.6 billion], then Hidroituango will also cost double [the original estimate], COP$20 trillion [US$5.2 billion]. The Comptroller General of the Republic (2019) asserted that Hidroituango will not make a profit in the next 120 years if it costs more than COP$15 trillion [US$3.9 billion],” Perez claims.

However, that Comptroller report actually found potential cost overruns totaling US$1.7 billion, not the US$3.9 billion that Perez attributes to the Comptroller report (see Medellin Herald November 14, 2019, “Colombia’s Controller-General Probing 2 Former Medellin Mayors, 2 Former Antioquia Governors over Hidroituango Errors, Financial Losses.”)

“If the new [EPM] Board does not take drastic measures, EPM will not belong to the people, EPM will belong to the creditors,” Perez concludes.

Ironically, it was Perez himself who last year suggested that EPM should buy-out the Antioquia government’s 53% share in the Hidroituango project, which either would drastically increase EPM’s debt burden or else force massive asset sales, thus hindering its capacity to tap debt markets for future, potentially profitable expansion plans.

EPM Response

Contradicting the Perez claims, EPM on August 20 filed a detailed response with Colombia’s Superfinanciera oversight agency. Below is EPM’s response, reproduced here:

“EPM, a solid and continuously growing company, was created in 1955, and for more than 50 years its target market was limited to Medellín and neighboring municipalities. This stage allowed the consolidation of a solid public service company, which became the engine of development in the region,” according to the filing with Superfinanciera.

“In 2006, the company began a process of transformation from the then-local business model to a Grupo Empresarial (Grupo EPM) structure, which was supported by internal analysis, external consultancies that established an organic and inorganic growth plan, which among other objectives sought diversify its portfolio, both in markets and in the incorporation of new lines of business, respecting its central axis as a provider of public services and thus responding to a changing environment.

“The transformation process was based on the need to diversify risk levels, establish a financial structure that would take advantage of the organization’s debt capacity and that would allow it to generate higher revenues for its owner, the Municipality of Medellín — a situation that to date has materialized with [profit] transfers that are made annually to its owner and that are vital for the social investment and well-being of thousands of people.

“The growth path outlined obliges the company to change the traditional financing structure of its own resources and establish financing schemes where debt is an important leverage of growth, generating a change in the composition of liabilities to equity, and growth in the total assets of the company. It is important to note that as of 2009, and in response to the demands of the international financial markets, EPM began the consolidation of the Group’s financial statements.

“The defined financing scheme requires a greater presence of EPM in the national and international financial markets, which have trusted in its ability to meet its obligations, a situation that has been evidenced in a history of good relations, which has been maintained even in critical moments such as the contingency of the Hidroituango hydroelectric project.

“The demonstration of this is reflected in the ratings given by the rating firms.

“2007: Since 2007, the rating of the Public Debt Bonds issued by EPM had a ‘AAA’ rating by Duff and Phelps de Colombia S.A., today Fitch Ratings.

“2009: Successful bond issues since 2007, initially in the local market. As of 2009, EPM ventures into the international capital market and on that occasion it obtained a ‘Baa3’ and ‘BB+’ rating by Moody’s and Fitch, respectively, which were very positive risk ratings for a newcomer issuer in the international capital market.

“2011-2020: In 2011, the company achieved a risk rating in the investment grade category ‘Baa3’ by Moody’s and ‘BBB-‘ by Fitch Ratings. Successively, in the following issues carried out in 2014, 2017, 2019 and 2020, it obtained ratings of ‘Baa3/BBB, ‘Baa2/BBB +,’ ‘Baa3/BBB’ and ‘Baa3/BBB’ granted by Moody’s and Fitch Ratings respectively — always maintaining the Investment Grade category and sometimes exceeding the country risk rating.

“Local and international banks, as well as multilateral banks have been very important actors in financing the investment, expansion and replacement plans of the company, which have been undertaken to guarantee the quality, timeliness and efficiency in the provision of the services of energy, water, sanitation, cleaning and natural gas for the entire community, mainly in Medellín, Antioquia and Colombia.

“The optimal levels of financial indebtedness are basically linked to the ability of companies to generate the cash flow required to meet financial obligations, a principle that EPM has honored and which is reflected in the fulfillment of all its obligations. The main source of resources for EPM is generated from the operation of the core businesses and the dividends delivered by its subsidiaries.

“Between 2006 and 2019, EPM has received from its affiliates and subsidiaries resources totaling COP$6.1 trillion (US$1.59 billion), of which the controlled companies have paid dividends and others totaling COP$3.5 trillion (US$912 million) and the non-controlled companies totaling COP$2.6 trillion (US$678 million).

“The resources that EPM generates annually have clear applications and are mostly used to guarantee the continuity of public services and fulfill the obligations with different stakeholders. Many of them are the result of changes derived from regulatory frameworks and business dynamics that are different from those of 20 years ago.

“The resources that have been allocated to the Hidroituango project as of June 2020 amount to COP$11.8 trillion (US$3.07 billion). The financing of the total investment has been provided resources totaling COP$5.8 trillion (US$1.5 billion) of debt and the rest from its own resources. Once the project has all its installed capacity (2.4 gigawatts), it is expected to generate an [annual] EBITDA of COP$1.3 trillion (US$339 million) on average.

“EPM is an important taxpayer in Colombia. In the last four years it paid approximately COP$1.7 trillion (US$443 million) in taxes, fees and contributions. It is important to note that, prior to 2006, EPM was a non-taxpayer, thanks to the tax exemption of power transmission and generation activity, an aspect that no longer is in force.

“Transfers to Medellin: EPM has become a lever for the development of Medellín and the quality of life of its inhabitants, through the transfers it makes to the Municipality. Thus, in the 2006-2020 period, surpluses have been delivered to the Municipality of Medellín totaling COP$13.3 trillion (US$3.47 billion) and additional resources totaling COP$2 trillion (US$521 million) were delivered from the UNE-Millicom merger and the sale of Isagen shares.

“EPM’s assets have grown in recent years by 251%, with a significant percentage in property, plant and equipment. [As a result], the company’s equity grew by 111%, increases that have been achieved thanks to a better financial structure and resources generated by business.

“The internal generation of funds and dividends allows estimating that the company could be paying its financial debt in a period of approximately four years. It is important to note that EPM is currently in a period of heavy investments in all its businesses, whose remuneration in accordance with regulations can take between 30 and 40 years, which allows projecting higher cash flows in the future,” the company concludes.